Busting the 20% Down Payment Myth

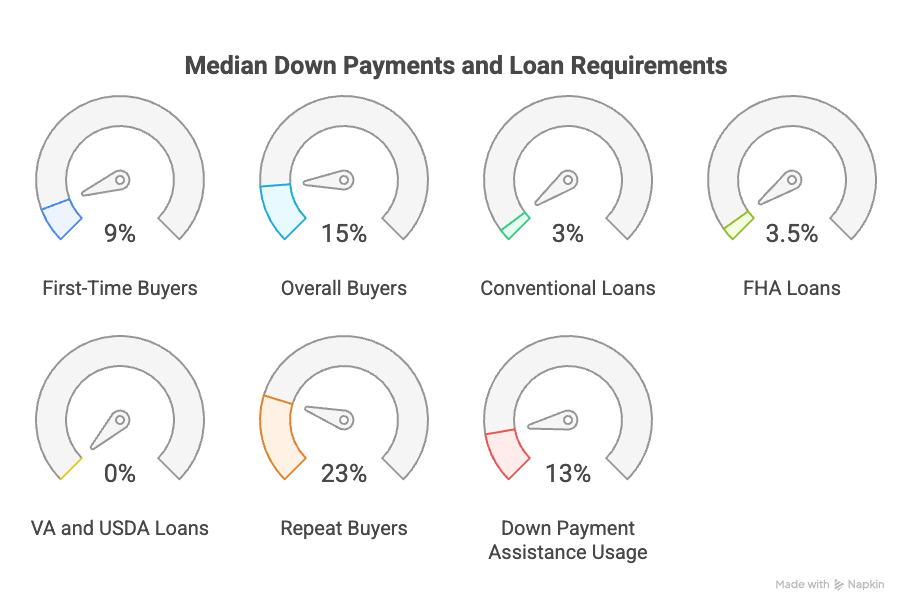

You probably don’t need a 20% down payment unless you’re trying to make your offer more competitive. Most buyers put down much less and still qualify for financing. Programs like FHA, VA, and USDA loans make homeownership accessible with minimal upfront cash. Recent national data shows the median down payment is around 9% for first-time buyers, and 15% overall—well below 20%.

What Typical Down Payments Look Like in 2025

Here’s how various loan types line up with minimum requirements and real-world patterns:

-

Conventional loans: require as little as 3% down for qualified buyers, although many choose 5%–10% or more

-

FHA loans: allow 3.5% down with credit scores above 580

-

VA loans: offer 0% down for eligible veterans and service members, with no private mortgage insurance

-

USDA loans: also provide 0% down for qualified buyers in eligible rural and suburban areas

-

Jumbo loans or second-home purchases: generally require 20%–25% down, but vary by lender

How Down Payment Assistance Changes the Picture

-

Nearly 80% of first-time homebuyers qualify for down payment assistance programs

-

Yet only around 13% actually use these programs

-

These resources often offer average benefits of $17,000, cutting the amount needed to save

Why Buyers Still Pay Higher Down Payments

-

Repeat buyers average around 23% down, or roughly $91,632, compared with 9% ($35,856) for first-time buyers

-

Some buyers still prefer 20% down to eliminate mortgage insurance, reduce monthly payments, or make their offer more appealing

-

Investors or second-home purchasers typically put down 20%–25%, depending on financing terms

How Colorado Buyers Benefit from Lower Down Options

-

Lower-down loans allow many Colorado buyers to enter the market sooner, especially in price ranges around $300,000–$600,000

-

Access to assistance programs makes that path even more realistic without delaying homeownership

-

Veterans, rural buyers, and many repeating buyers can still qualify with no or minimal down payment

How Corken + Company Guides Buyers on Down Payments

We offer:

-

Clear alignment of loan options—conventional, FHA, VA, USDA—with realistic down payment thresholds

-

Referrals to lenders who help assess whether assistance programs apply and how to access them

-

Strategic advice about when it makes sense to save more versus when buying now adds more long-term value

Summary of Down Payment Insights

-

Myth: you must put down 20%—most buyers do not

-

Median down payment: 9% for first-time buyers, 15% overall

-

Conventional loans: minimum around 3%; many buyers use 5%–10%

-

FHA loans: require 3.5% down for scores above 580

-

VA and USDA loans: often need 0% down for eligible applicants

-

Repeat buyers: median down payment is 23%, or roughly $91,632

-

Down payment assistance: nearly 80% qualify, only about 13% use; average benefit ~$17,000

You don’t need to wait years to save up a large down payment in 2025. But understanding your options—loan types, assistance programs, and strategic tradeoffs—is essential. That’s where Corken + Company helps. We connect Colorado buyers with smart financing options, expert partnerships, and local guidance so you can move forward with confidence. Visit www.corken.co or call 303‑858‑8003 when you’re ready to get started.