How Credit Scores Affect Your Home Buying Journey

Many buyers overestimate the credit score they need to qualify for a mortgage. According to Fannie Mae, about 90% of prospective buyers think they need better credit than they actually do.

Lenders look at your overall financial profile but your credit score remains a key factor—not just for approval but also to determine interest rate and loan terms.

Minimum Credit Scores by Loan Type

Here’s how various loan options align with typical requirements:

-

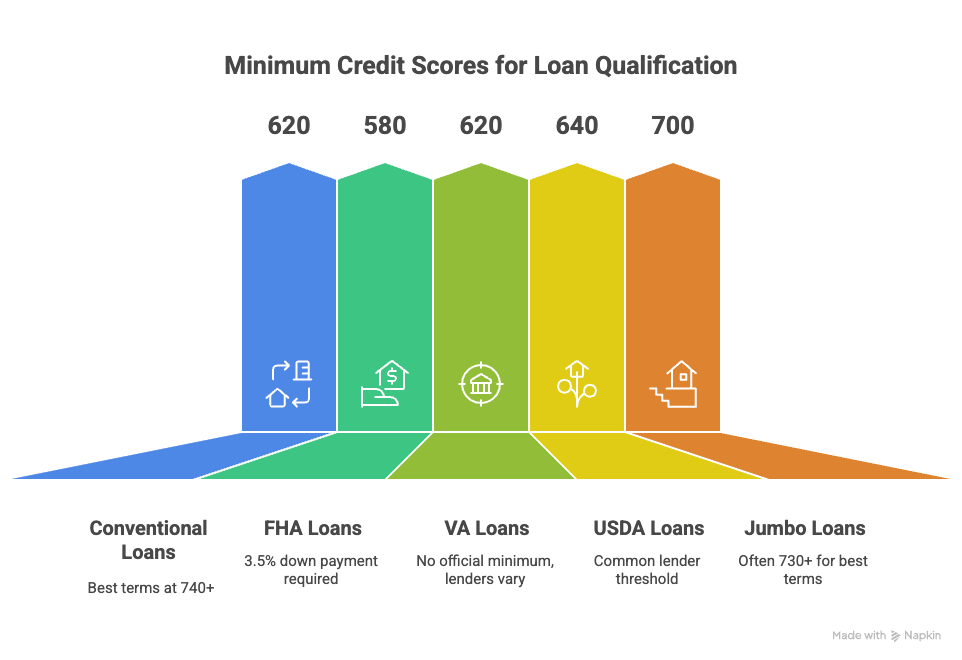

Conventional loans usually require a minimum score of 620, though qualifying scores of 740 or above unlock the lowest interest rates and most favorable terms.

-

FHA loans allow scores as low as 580 with a 3.5% down payment or 500–579 with 10% down.

-

VA loans have no official minimum, but most lenders prefer a credit score of 620 or higher, though some accept loans with scores in the 500s.

-

USDA loans typically require a credit score of 640 or higher, though there is no firm minimum.

-

Jumbo loans generally demand a credit score of 700 or above.

What Happens When Your Credit Score Is Lower

-

Borrowers with scores between 580 and 620 may qualify for FHA loans, though usually require a larger down payment and higher mortgage insurance.

-

Buyers with scores under 580 face higher interest rates, larger down payments, and fewer lender options. FHA is often the most viable path—but terms will be less favorable.

-

Higher scores translate to more loan programs and lower interest rates, which can amount to thousands in savings over a 30-year term.

Why a Higher Score Pays Off

-

Moving from the low 600s to high 700s can reduce your mortgage rate and save you significantly in monthly payments.

-

Lenders often will only approve certain programs for buyers with strong credit and income profiles, even if the base requirement is lower.

Emerging Shift: Expanding Credit Access with VantageScore

Recent policy changes now allow Fannie Mae and Freddie Mac to accept VantageScore 4.0 for loan qualification. This includes rent, utility, and telecom history in credit evaluation—helping more Americans No longer excluded due to lack of traditional credit.

What’s Creditor Expectations Today in Colorado

-

Most conventional loans require at least 620, with excellent rates available from scores of 740+.

-

FHA offers flexibility for scores of 580+ or even 500–579 with higher down payments.

-

VA and USDA loans present options with 620+ typical thresholds (though some lenders go lower).

-

Jumbo financing often needs 700 or higher scores.

How Corken + Company Helps Buyers Navigate Credit Complexity

-

We connect you with local Colorado lenders who clarify real expectations and rate scenarios.

-

We help align your target loan type with realistic credit strategy and planning.

-

We refer trusted professionals who can advise on credit improvement steps if needed.

-

We position your offer effectively—even if your score is not perfect—based on loan structure and landlord flexibility.

Credit Score Summary

You don’t need a perfect credit score to buy a home—but better credit improves your borrowing power, lowers monthly payments, and expands your options. Whether you’re exploring conventional, FHA, VA, or USDA financing in Colorado—Corken + Company connects you with knowledgeable agents and lender partners to chart the right path forward. Visit www.corken.co or call 303‑858‑8003 to get credit-smart homebuying guidance.