Turbulence in stock markets sent jitters through the economy. The more than 2000-point drop in the Dow Jones Industrial Average in early-February raised investors’ nervousness, and market volatility jumped. Are these just bumps in the road for a booming economy with high production, employment and income? Let’s check some key features.

Bull Markets

Worry lists grow during long upswings as anxiety builds about inflation, asset values, borrowing costs and speculation, among other things. Next month, the current 106-month expansion ranks second longest behind 1991-2001 (120 months). With the ride up approaching nine years, it’s not unreasonable to be cautious about financial markets, where pressures can develop early. Worries intensify with uncertainties about national policies and global conditions.

Inflation

The consumer price index (CPI) rose 2.1% last year; its broader counterpart, the personal consumption expenditures index (PCE), advanced 1.7%. These are far from high-pressure surges. They are also close to the 2% target set by the Federal Reserve.

Interest Rates

Households and businesses face higher borrowing costs as the Federal Reserve reduces monetary stimulus and raises interest rates. The federal funds rate, for example, an overnight borrowing charge among banks, hit 1.42% in February, up from 0.66% a year ago. For non-financial businesses, the 90-day commercial paper rate is now 1.69% compared to 0.77% last year. Loan rates on autos are climbing slowly, as are mortgage interest rates, now close to 4.5% for 30-year conventional loans.

Speculation

Speculative actions generate unease, especially when financed with borrowed funds. The bitcoin value, for example, hit a high in late-2017, and then plunged more than 50%. Some banks now prohibit credit-card purchases of such highly speculative cryptocurrencies. “Fear of missing out” does draw more investors toward higher, riskier returns. Speculation, however, is not as intense as it was in the subprime mortgage market a decade ago.

Stress

Despite perplexing volatility of stock markets, the Federal Reserve Bank of Kansas Csity (FRBKC), which includes Colorado in its district, reported subdued financial stress as 2018 began. In the FRBKC’s March report, the stress index, measuring yields and asset prices nationwide, remained below its long-term average.

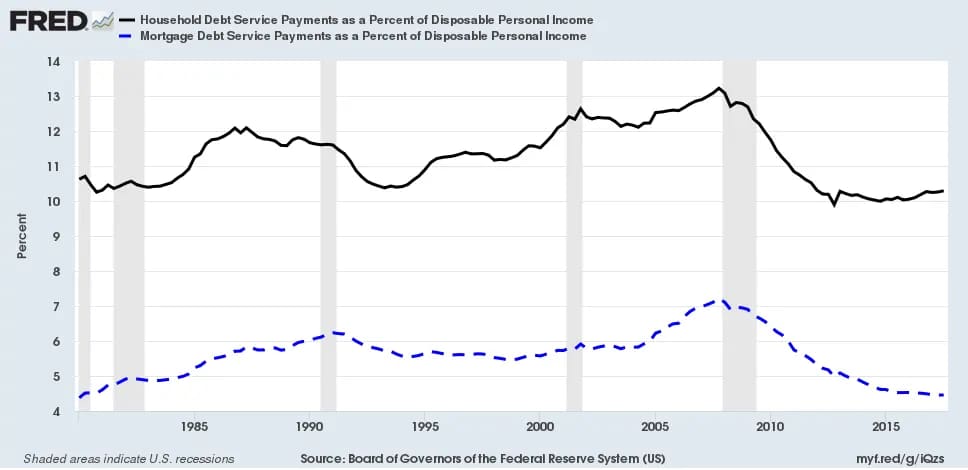

Life and Debt

Increasing house values continue to improve owners’ net worth. That wealth gain and rising income support consumer spending. Moreover, household debt service hovers near 10%, after hitting a high of 13% in 2007 (see chart). Following years of deleveraging, consumers are in good shape and optimism prevails.

Local Highlights

Denver metro’s income has increased 36% and 20% faster than the nation and the U.S. western region, respectively. The table shows Denver’s lower rank in expenditures for owner-occupied and rental shelter compared to select western metro areas. While financial fluctuations may impact portfolios, they are unlikely to change strong conditions here. Global trade restrictions threaten, however. Tariffs on Canadian lumber, for example, are already having negative impacts on homebuilders.

*Owned dwelling expenses include mortgage interest and charges, property taxes, maintenance, insurance, etc.*

Source: U.S. Department of Labor, Bureau of Labor Statistics, Consumer Expenditure Survey.

Dr. Paul Kozlowski is professor emeritus of business economics and finance at the University of Toledo and has served as an advisor to business and government organizations for over forty years. He is past-president of the Mid-Continent Regional Science Association and his articles appear in a variety of economic journals and books. He holds a Ph.D. in economics from the University of Connecticut and lives in Denver.