The data confirms that the Denver Metro area is no longer in a shifting market. Instead, it has shifted, and the real estate market is more balanced.

Month-over-month, the market is down 3.33 percent but compared to last year, it is still up 11.04 percent, indicating that a more balanced market, combined with slightly decreasing interest rates, may create opportunity for those who previously felt burned out on the process.

One of the primary indicators of a shifted market is the close-price-to-list-price ratio, which was down to 100.81 percent. Buyers have become more specific about what they are looking for and frequently question if, and how much, below the asking price they can offer. Gone are the days when a seller could simply put a sign in the yard and expect their home to sell.

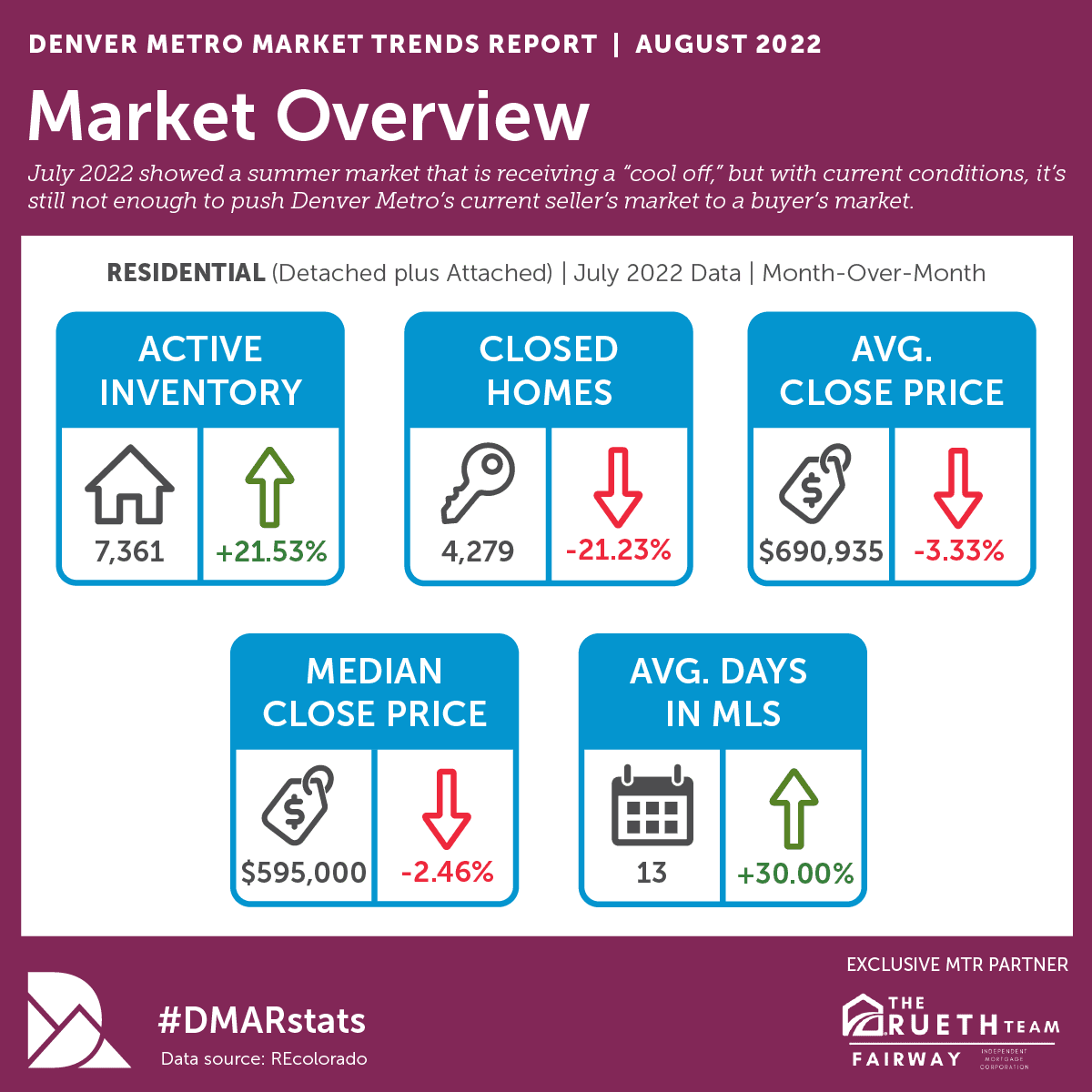

Every indicator points to the market shifting closer to a buyer’s market. The month-end active listings increased 21.53 percent last month. Pending and closed deals decreased and days in the MLS increased by exactly 30 percent. However, the market is still far from what many experts would consider a buyer’s market. There are over 2,000 fewer properties on the market today than there were three years ago and, during the last three years, the amount of standing inventory peaked in June and July, which was abnormal. Historically, the market doesn’t peak until August or September.

Year-to-date, the entire market has seen 7.18 percent fewer homes closed than the previous year. Even with fewer purchases, the market has transacted over $1 billion more in sales volume than the previous year, indicating how high prices have soared from the previous year. This is also indicated in the close-price-to-list-price ratio of 105.33 percent, down from the previous month.

DMAR’s monthly report also includes statistics and analyses in its supplemental “Luxury Market Report” (properties sold for $1 million or greater), “Signature Market Report” (properties sold between $750,000 and $999,999), “Premier Market Report” (properties sold between $500,000 and $749,999), and “Classic Market” (properties sold between $300,000 and $499,999).

With many people out-of-town, combined with mortgage rates that briefly went over six percent, the Luxury Market also felt the seasonal cooling in July. New listings were down 22.13 percent, pending sales were down 18.16 percent and closed homes were down 30.80 percent since June. There were 718 new luxury listings in July and 492 closings.

At the end of the month, there were 1,190 active homes for sale in the Denver Metro area over $1 million signifying that luxury inventory is up. Compared to last year, inventory has increased 39.05 percent, with most of that in detached homes. Notably, the months of inventory increased in July to 2.37 months for detached luxury homes and 3.31 months for attached. This is a leading indicator that the Luxury Market, particularly attached luxury homes, is no longer an extreme seller’s market as the Denver Metro has seen for the past two years. The Luxury Market saw the highest number of expired listings, at 183, of any sector in July. This trend toward a balanced market is reinforced by the close-price-to-list-price ratio for July, which was down 3.11 percent from the prior month to 100.44 percent.

“Just as July gives us some breathing room to travel and enjoy our summer vacations, it brings buyers in the market some breathing room with longer showing windows, more time to consider making an offer, less competition, and slowing prices,” said Colleen Covell, DMAR Market Trends Committee member and Metro Denver Realtor®. “Sellers, meanwhile, need to appreciate this shift in the landscape and adjust their expectations. Many homes are not going under contract in the first week, there will be under ask price offers and contingencies won’t be waived. Just like it used to be, pre-pandemic! All-in-all, a return to normal is on the horizon this year.”